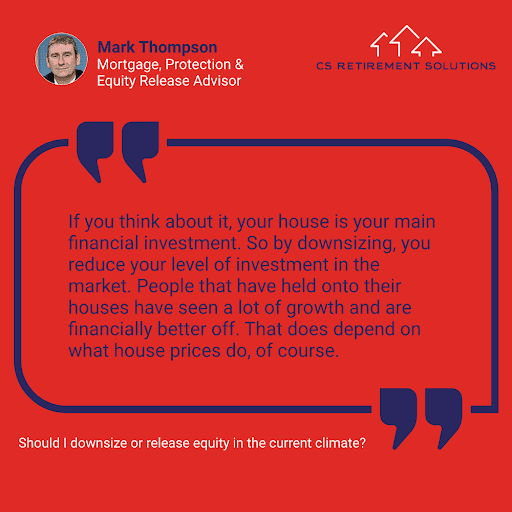

Protected: Should I Consider Downsizing Or Releasing Equity During The Cost Of Living Crisis?

There is no excerpt because this is a protected post.

Saving For A Pension 2023

Saving For A Pension 2023 Jamie Benn, Financial Advisor at CS Financial Group talks us through pensions and how to save for the future. Will